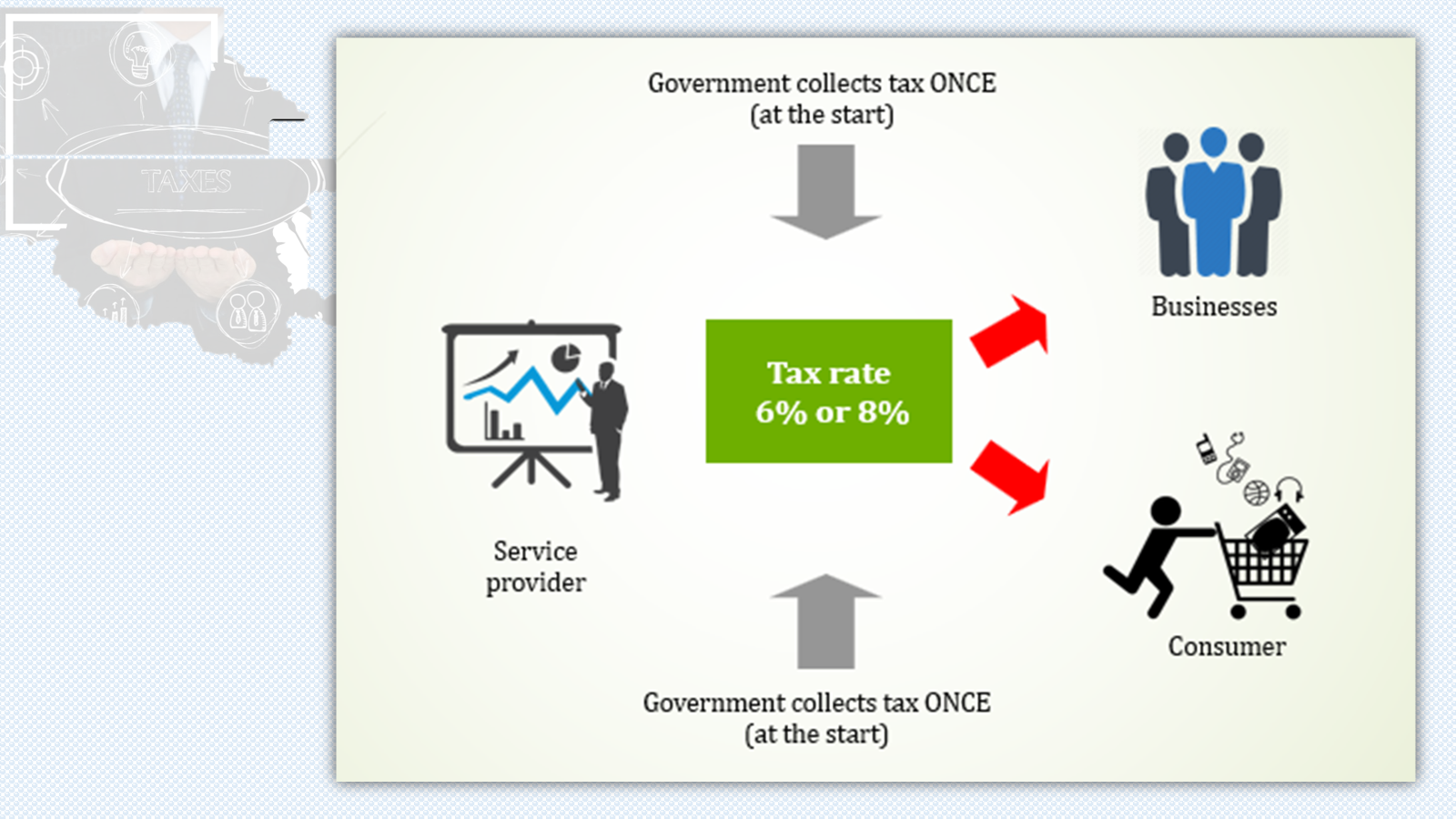

Service tax is a tax charged on:-

i. any provision of taxable services;

ii. made in the course or furtherance of any business;

iii. by a taxable person; and in Malaysia.

Taxable person is a person who provides taxable services in the course or furtherance of business in Malaysia and is liable to be registered or is registered under the Service Tax Act 2018.

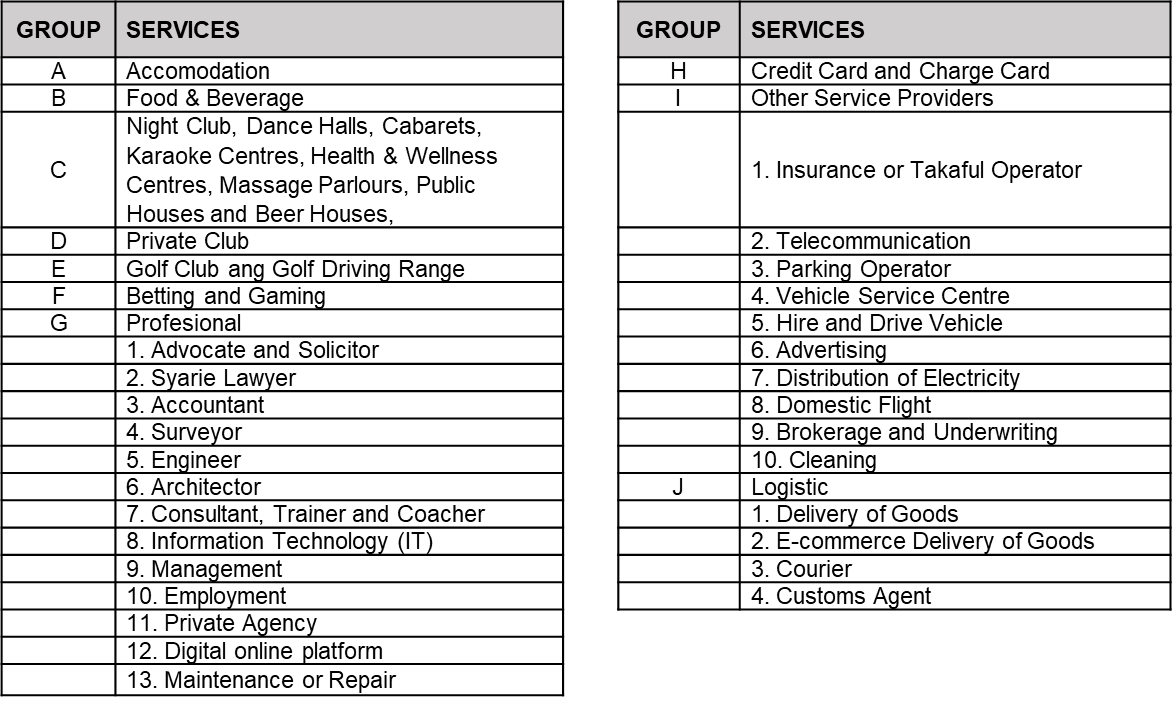

i. The tax rate is 8% for all taxable services except;

ii. F&B, Logistics, Telecommunications, and Parking are at a rate of 6%.

iii. RM25 for credit card / charge card.

The threshold value is determined through 2 methods:

(a)Historical method

The backward method is based on the value of taxable services for any month, combined with the value of taxable services for the 11 months preceding that month.

Example: Value of Services from July 2024 to August 2023.

(b)Future method

The forward method is based on the value of taxable services for any month, combined with the value of taxable services for the 11 months following that month.

Example: Value of Services from July 2024 to June 2025.

The provision of food services by any cafeteria is subject to service tax if the sales value of the services provided exceeds RM 1,500,000.00.