Sales tax is a tax charged and levied:-

- on taxable goods manufactured in Malaysia by a taxable person and sold, used or disposed by him;

- on taxable goods imported into Malaysia.

Sales tax is not charged on:-

- goods listed under Proposed Sales Tax (Goods Exempted From Sales Tax) Order;

- Certain manufacturing activities are exempted by Minister of Finance through Proposed Sales Tax (Exemption from Registration) Order.

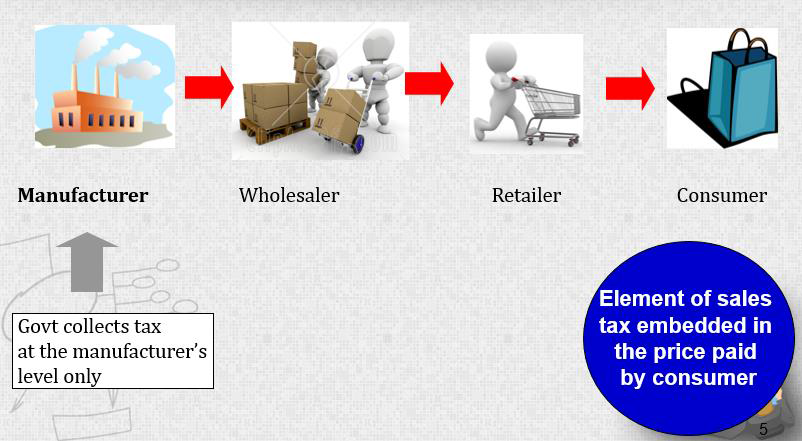

How Sales Tax Works?

Taxable Person

Taxable person is a person who manufactures taxable goods and is:-

- liable to be registered

- Reached sales threshold

- Manufacturer — RM 500,000.00

- Sub-contractor — RM 500,000.00

- registered under Sales Tax Legislation

- Mandatorily registered

- Voluntarily registered

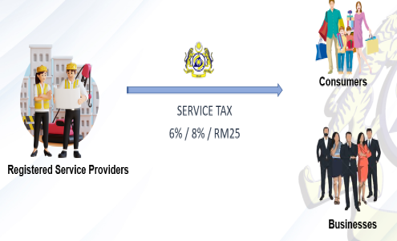

Service tax is charged:-

How Service Tax Works?

How Service Tax Works?

-

taxable services;

-

provided in Malaysia

-

by a registered person carrying on his business

-

imported taxable services (c.i.o 1 January 2019)

-

Any person providing taxable services liable to be registered if the total amount of taxable services provided by him in 12 months exceed threshold.

- 6% (from 1 September 2018 to 29 February 2024)

- 8% (effective from 1 March 2024), except for food and beverage (F&B) services, parking services, logistics, and telecommunications services, which remain at 6%.

- Provision of credit card or charge card services:

- A specific tax rate of RM25 is imposed on the issuance of a principal card or supplementary card, and for every subsequent year or part thereof.

- Effective from 1 July 2025, the scope of Service Tax has been expanded to include the following new services:

-

- Rental or leasing services – 6% (effective from 1 January 2026)

- Construction work services – 6%

- Financial services – 8%

- Private healthcare services – 6%

- Education services – 6%

How Service Tax Works?